WSFS Bank Visa Debit Card

A WSFS Bank Visa Debit Card allows you to shop, pay bills online or withdraw cash from ATMs whenever you need it. Works like cash with the power of Visa behind it.

Pay With Confidence and Ease

Check out quickly and securely

Enjoy the convenience and security of contactless payments and chip technology

$0 liability protection

Feel secure knowing you will never be held responsible for unauthorized charges made with your card[1]

24/7 fraud alerts

We help to protect you by immediately alerting you of potential fraud on your debit card through two-way texts, phone calls and email alerts

Card controls

With our WSFS Mobile App, lock and unlock your card, control where it can be used and establish threshold amounts

Pay with your mobile phone

Easily add your card to your digital wallet – PayPal®, Apple Pay® and Samsung Pay®

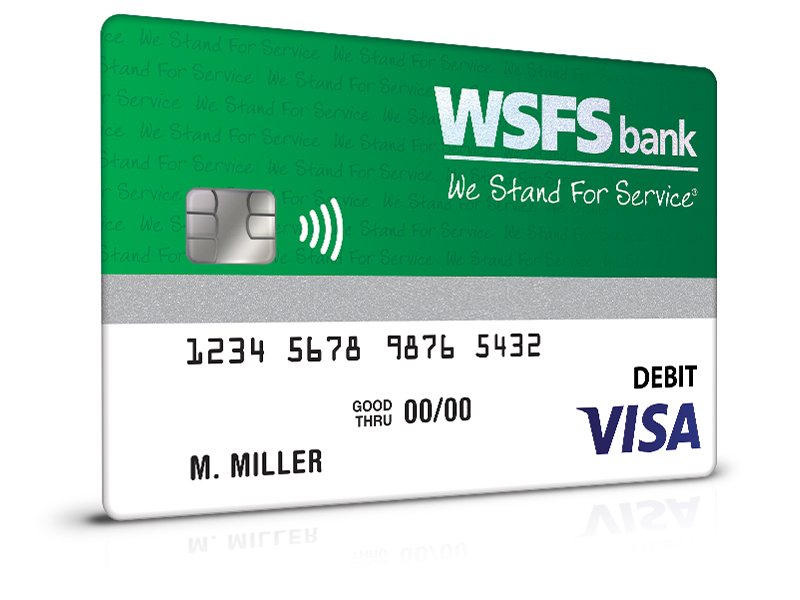

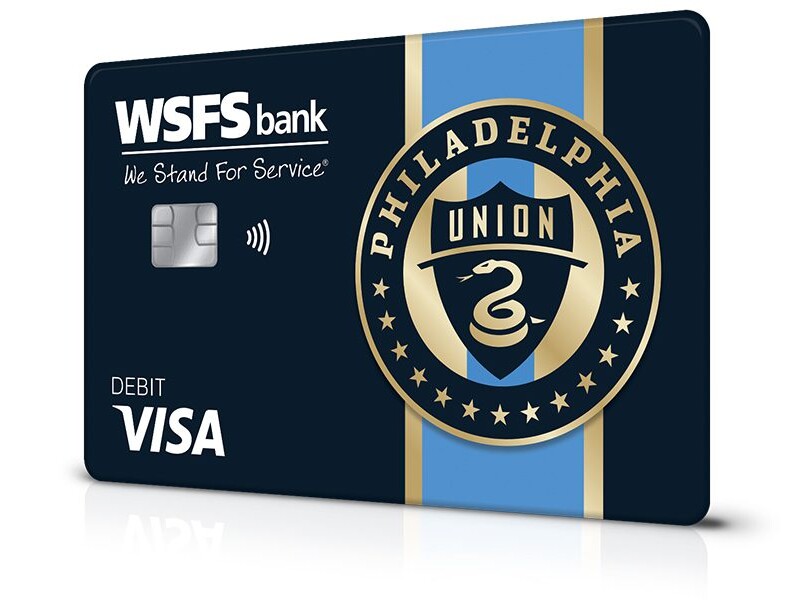

Choose From Two Designs

WSFS Bank Visa Debit Card

Standard WSFS Bank branded debit card.

Philadelphia Union Visa Debit Card

The debit card for those who DOOP! Support the squad and show off your Philadelphia Union pride every time you make a purchase.

Contactless – The Easy and Secure Way to Pay

Sometimes referred to as “Tap to Pay,” contactless payments use short-range wireless technology to make secure payments between a contactless card and a contactless-enabled terminal, providing the ability to “tap” the terminal to pay—without the need to swipe or insert your card. Next time you make a purchase, follow these 3 simple steps:

Help Your Children Learn to Earn, Save, and Spend Wisely

Greenlight puts kids and teens on the path to lifelong money management skills.

What is Greenlight?

Greenlight is a free[2] financial education app and debit card designed specifically for kids and teens to use, all under parental supervision.

Parental Controls

Parents receive real-time spending notifications, can quickly send money to their child’s card, set spending limits by category, and more.

Real-life Financial Skills for Kids

With their own debit card, kids learn the value of earning and saving – and have fun along the way.

Your WSFS Checking Options

Everyday Banking

Our most popular account is designed to meet everyday money management needs.

Campus Banking

Bank on your future with a WSFS Campus Banking account providing several benefits that let you focus on what matters most, your education and well-being.

Relationship Checking

A checking account with a wider range of benefits that rewards a deeper relationship with WSFS.

Questions?

Our friendly Associates are here to help 7am-7pm (M-F) and 9am-3pm (on weekends) at 888.973.7226, by scheduling an appointment or visiting the nearest WSFS Banking Office.

Recent Articles

-

- Article

-

- Article

-

- Article