A dollar today does not represent a dollar tomorrow. Inflation is the cause of that fact. Traditional measures of inflation have depicted a lower rate of inflation over the past 20 years. However, measures used by the government agencies are missing other forms of price increases that cannot be ignored and should be considered. These traditional measures are used by the Federal Reserve to implement interest rate policy. By continuing to ignore other forms of inflation, the Federal Reserve runs the risk of appeasing the fiscal government and harming future generations.

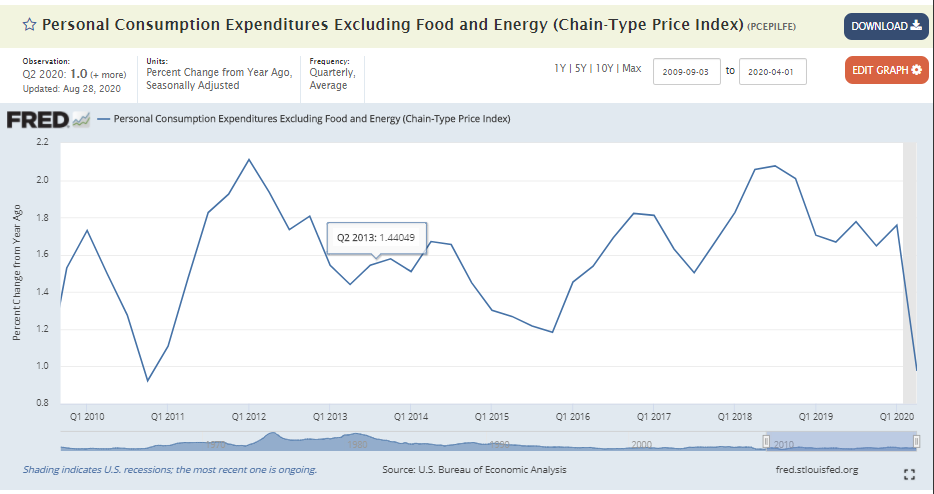

Inflation is the increase in the price of goods and services over time. One typical driver of inflation is an increase in production costs such as raw materials and wages. Another one is a surge in demand for products and services making consumers increase their willingness to pay more for a product. With those concepts in mind, traditional statistics to measure inflation are CPI and PCE (personal consumption expenditures). The PCE deflator is the preferred measure of inflation for the Federal Reserve Bank. If you look at a chart of the year over year percentage change in PCE ex food and energy, you can see it has been below 2% for over a decade.

(Source: https://fred.stlouisfed.org/series/PCEPILFE)

A lot has been said about the latest notification by the Federal Reserve of letting inflation run higher than its usual 2% target and utilizing more of an average 2% inflation target. One can argue that the Federal Reserve is creating inflation in asset prices above that 2% hurdle rate and it is those asset inflation rates that is proving to be beneficial to the wealthy population at the expense of future generations. CPI does not measure investment inflation, or returns, as they deem those factors to be outside of the consumption arena. According to the BLS (Bureau of Labor Statistics) website, they factor in rents instead of home purchases into their calculation for CPI, reasoning described in one of their own factsheets, “Housing units are not in the CPI market basket. Like most other economic series, the CPI views housing units as capital (or investment) goods and not as consumption items. Spending to purchase and improve houses and other housing units is investment and not consumption. Shelter, the service the housing units provide, is the relevant consumption item for the CPI. The cost of shelter for renter occupied housing is rent. For an owner-occupied unit, the cost of shelter is the implicit rent that owner occupants would have to pay if they were renting their homes.”[1] The median sales price for homes sold in the country has gone from $165,300 in Q1 2000 to $313,200 in Q2 2020, representing an approximate 3.2% annual increase.[2] Likewise, the S&P 500 has realized a 6% total return annual increase from that same time period.

Persistently low rates produce a wealth effect for the current population, generally propping up asset prices. The middle aged to older generation can reap those benefits through savings and retirement plans. However, the younger generations must experience wage growth that matches those asset inflation rates in order to keep up with the standard of living of these past generations. Only time will tell how this plays out, but by ignoring the asset inflation and only focusing on traditional measures of inflation the Federal Reserve could be playing a dangerous game.

Recent Articles

Navigating a tax bill can be stressful but falling victim to a scammer while you’re trying to resolve it is…

With tax season underway, many business owners are gathering documents, reviewing financial records, and working toward filing their returns. While…

Welcoming a new baby is one of life’s most exciting milestones. It’s a time filled with joy and anticipation, but…

Helping you boost your financial intelligence.

Read our financial resources from your friends at WSFS.