Long Growth Stocks Equals Increased Interest Rate Risk

Duration is a term used in fixed income investing. It is a measure of interest rate risk that a bond or fixed income strategy has. Bond prices and interest rates move inverse to each other; thus, interest rate risk is the potential reduction in the value of a bond if interest rates move higher. The longer the duration, the larger the loss.

What some investors don’t realize is the same interest rate properties can be extrapolated to equity investing.

Equities are generally used as long duration assets. The entire basis for stock investing is to receive partial ownership of the future cash flows of a company in perpetuity. Companies utilize those cash flows to pay a dividend, buy back stock or reinvest in their own business for growth reasons.

With that in mind, the typical method used by portfolio managers and analysts for assigning a value to those perpetual cash flows is a discounted cash flows model. Future cash flows are projected and then discounted back to the present to arrive at an intrinsic value, or present value, of a company. This is where interest rates play an enormous part in equity investing. The discount rate primarily consists of a risk-free rate (Treasury Rate) and an equity risk premium; the equity risk premium is the excess return generated over the risk-free rate and compensates the investor for taking a higher level of risk.

Lower discount rates produce higher equity values; however, the effects vary by equity styles. The two primary equity styles are growth and value stocks. Growth stocks are typically companies that have experienced high growth rates in revenues and earnings over a certain period. Value stocks are usually companies that are trading at cheaper valuations than their historical average or the overall market.

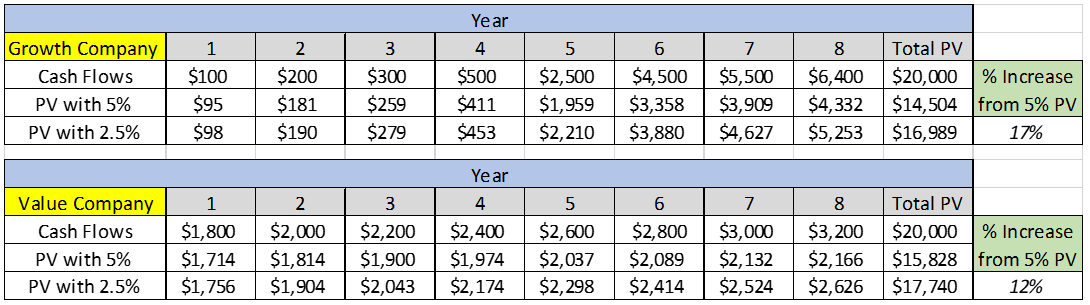

The traditional path of cash flows for these two distinct types of companies are different. Value stocks generally have more mature cash flows that are growing at low, steady rates, while growth companies typically produce little to no positive cash flows in the beginning of their life cycle but eventually generate large cash flows later in their life cycle. The effect of utilizing a lower discount rate on each type of company can be seen in a simple example below.

The two hypothetical companies have the same total future projected cash flows, but the growth company’s cash flows are smaller in the first few years and then increase substantially in the latter years. As seen in the example, a lower discount rate, results in a sizeable increase in the present value for the growth company versus the value company; making them look more attractive to most investors.

Consequently, we could hypothesize a move lower in interest rates would result in growth stocks outperforming value stocks and vice versa; that has been the case during two distinct periods of time within the last 14 months.

The charts below display the ratio of the Russell 1000 Value ETF (Symbol: IWD) divided by the Russell 1000 Growth ETF (Symbol: IWF) versus the 5-year Treasury yield. At the height of the pandemic, interest rates plummeted and so did the value ETF relative to the growth ETF. Since the beginning of Q4 2020, interest rates have steadily climbed higher and we have seen that dynamic reverse. Based off these charts, in the short term, it is evident that changes in interest rates generally have a significant impact on the relative performance of growth and value stocks.

Remember, interest rate risk is the potential loss in value of a bond if interest rates move higher. In the example above, the effect of interest rates on growth stocks versus value stocks is evident. Connecting the dots, a portfolio that is overweight in growth stocks has an elevated level of interest rate risk that some investors may not realize. In essence, that type of equity portfolio is making an interest rate call, believing interest rates will continue to be lower. A balanced approach to the many styles of equity investing can alleviate risks that some investors may not even realize they are taking.

Recent Articles

-

- Article

-

- Article

-

- Article

Helping you boost your financial intelligence.

Read our financial resources from your friends at WSFS.