Safe Investment Considerations: Tips to Balance Your Portfolio

Many people are risk averse when it comes to investing. It’s natural to be wary of the volatility of the stock market and to want to protect your savings with a safer investment option. In the first quarter of 2020, the stock market “fluctuated” to a loss of almost -20%. Even though the stock market rebounded in the second quarter by a bit more than +20%, the unrelenting math of compounding still produced a loss of just over -4% for the first half of the year.

As Mark Twain once put it, “I’m more concerned about the return of my money than the return on my money.” For investors who share that prudent mindset, Certificates of Deposit (CDs) and Money Market Accounts are familiar choices. These investment solutions are very safe and yield a higher rate of interest than a checking account. Certificates of deposit have been popular for many years because they offered both safety of principal and a modest return to individual investors.

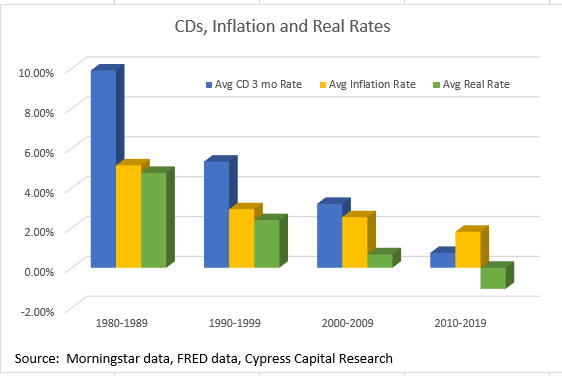

The 1980s and 1990s were a golden era for cautious savers. Back then, investors could buy Certificates of Deposit at attractive yields of as much as 5%-10%. That made CDs an excellent holding, because you could get (1) a completely safe CD, (2) an attractive nominal return of 5%-10% and (3) a nice “real” return of 2%-4% above the rate of inflation to boot. But in the last decade since the Global Financial Crisis of 2007-2009, CD rates have declined meaningfully, as shown by the blue bars below:

The chart shows the average 3-month CD rate in blue, the average inflation rate in yellow and the average real rate in green for the four decades since 1980. Note that the average real interest rate is just the average 3-month CD rate minus the average rate of inflation for each decade.

The chart shows the average 3-month CD rate in blue, the average inflation rate in yellow and the average real rate in green for the four decades since 1980. Note that the average real interest rate is just the average 3-month CD rate minus the average rate of inflation for each decade.

CDs furnished solid average returns in the 1980s and 1990s, and even with lower rates in the first decade of the 21st Century the real return on CDs still remained positive.

Unfortunately, times change.

In the last ten years since the Global Financial Crisis, 3-month CDs provided an average yield of only 0.7%, which lags the average inflation rate of 1.8% by just over a percent.

Although a 1.8% increase per year in the cost of living appears benign in the short run, for the decade ending December 31, 2019, the purchasing power of a dollar fell by more than 16%. When inflation is persistent and the Federal Reserve keeps interest rates near zero, savers may need to choose between safety of principal that loses purchasing power over time and carefully taking on some risk to maintain the real value of their nest egg.

At present, the challenge for savers can be daunting. The COVID-19 coronavirus crisis of 2020 and easing of Federal Reserve policy have pushed short-term rates lower, and CDs now yield a mere 0.2%. With inflation expected to increase at 1%-2% over the next few years, cautious investors face a dilemma. Putting safety first and rolling over short-term CDs will ensure that the nominal value of their money is protected, but it’s likely that the real purchasing power of their savings may be eroded by inflation.

No one likes taking risk, but today, in the current era of coronavirus lockdowns and very low interest rates, investing for safety is a complex business. If you find 24/7 news cycles and volatile markets intimidating, why not find and ask a financial advisor for assistance?

Recent Articles

-

- Article

-

- Article

-

- Article

Helping you boost your financial intelligence.

Read our financial resources from your friends at WSFS.