Home Equity Line of Credit (HELOC)

Put the equity in your home to work. A Home Equity Line of Credit can provide access to cash to pay for home improvement projects, unexpected emergencies and more.

Imagine What’s Next

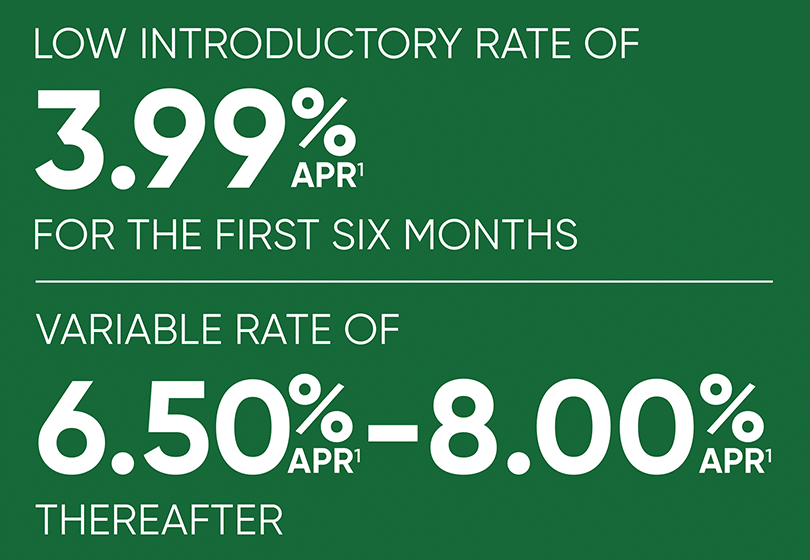

You’ve built more than a home-you’ve built equity. Now, put it to work with a WSFS Home Equity Line of Credit. Access flexible funds for your biggest plans and enjoy a low 3.99% APR* introductory rate for the first six months, with a variable rate of 6.50% APR* – 8.00% APR* thereafter.

Key Features of a Home Equity Line of Credit

Built-in Peace of Mind

A WSFS Home Equity Line of Credit is a flexible, revolving line of credit available to you when you need it. Lock in a fixed rate on all or a portion of your balance.[1]

Interest-Only Payments

You pay only the interest on the money you borrow for 10 years (draw period) from the date the line is established.[2]

Option to Lock Your Rate[1]

You can choose to fix the rate on all or a portion of your line, and keep accessing the rest of your available line of credit.

Included With Your Home Equity Line of Credit

Competitive Rates

Only pay interest on what you borrow while you put your line of credit to work.

Flexible borrowing

Access only the funds you need, up to your credit limit.

Easy access

Access your line of credit simply by writing a check or using a WSFS HELOC Access Card.

Online account access

View your loan balance, monitor transactions and make your loan payments.

Why Choose a Home Equity Line of Credit?

Here for All Your Personal & Business Banking

Step 1: Select line amount

Minimum line of credit available is $25,000. Maximum is $2,500,000.

Step 2: Provide documents

Once we review your application and your credit history, you may need to provide income documents.

Step 3: Loan processing

WSFS will verify your income and your home’s value.

Step 4: Closing and funding

Once approved, we will work with you to schedule your closing appointment when and where it is convenient for you.

FAQs

Other Products That May be Right for You

Check out these related products.

Home Equity Loan

Tap into your home’s value to finally embark on that big home project or purchase you’ve been eyeing.

Cash Back Visa® Credit Card

Earn unlimited cash back on everyday spending with our 3-2-1 Cash Back Program and 0% balance transfers for nine billing cycles.

Questions?

Our friendly Associates are here to help 7am-7pm (M-F) and 9am-3pm (on weekends) at 888.973.7226, by scheduling an appointment or visiting the nearest WSFS Banking Office.

Recent Articles

-

- Article

-

- Article